A profitable business can face serious cash flow issues because profit and cash are two different things. Profit appears on the income statement when work is delivered; cash only arrives when clients pay, often 30, 60, or 90 days later. Julia Delin, CEO and Co-Founder of Cheque, calls this the payment gap: the structural lag between earning revenue and receiving it that keeps even healthy service businesses perpetually short.

What are cash flow issues? Cash flow issues occur when a business cannot meet its financial obligations because money is not in the bank, even when the business is profitable. The most common cause in service businesses: the gap between when revenue is earned and when cash is received, which spans 30 to 90 days under standard payment terms.

About Julia Delin

Julia Delin is the CEO and Co-Founder of Cheque, a fintech company building payment infrastructure for small service businesses. Before founding Cheque, Julia worked in enterprise payment systems, the same infrastructure that processes accounts payable for Fortune 500 companies. That experience gave her a specific lens: the tools that have moved enormous volumes of enterprise payments for decades have never been made accessible to the cleaning company, the staffing agency, or the consulting firm. Cheque is built to change that. In this episode of Predictable B2B Success, Julia explains why cash flow issues are structural and how service businesses can fix them systematically.

Watch the Episode

Table of Contents

What Are Cash Flow Issues? (And Why Profitable Businesses Get Them)

A profitable business can run out of cash. Cash flow issues occur when a business does not have enough cash on hand to cover its obligations, including payroll, rent, and supplier invoices, regardless of how much revenue it is generating on paper.

The paradox that surprises most business owners: you can be profitable and still run out of cash.

Profit is a number on a document. Cash is what is in your bank account. These two figures can, and regularly do, diverge sharply in service businesses where clients pay on 30-, 60-, or 90-day terms.

In reviewing B2B service businesses, the gap between their P&L and bank balance is the single most consistent pattern encountered, and the most consistently misdiagnosed. Business owners treat it as a cash problem when it is really a timing problem.

Here is the mechanism. Your income statement records revenue the moment you issue an invoice. The cash from that invoice does not arrive for weeks or months. In the meantime, you still need to pay your team, your software subscriptions, and your rent. The expense clock does not pause while you wait for a client to process payment.

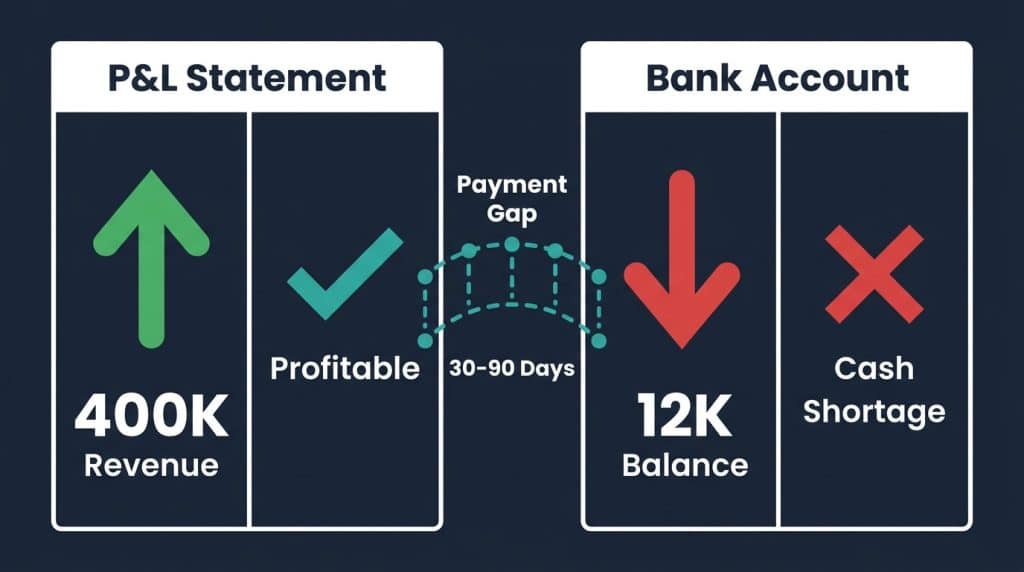

This is why a graphic design studio with $400,000 in annual billings can struggle to make payroll. The work was done. The invoices went out. The revenue is real. The cash has not arrived yet.

Research confirms this is not an edge case. According to a study cited by SCORE, 82 percent of small businesses that fail do so because of cash flow problems, not because of weak revenue or poor products (SCORE, 2019) The business was often profitable. The cash simply was not there when it was needed.

Direct Answer Block: The Profit-Cash Paradox

A profitable business can run out of cash because profit is recorded when work is completed, but cash only arrives when clients pay. In a service business operating on Net-30 or Net-60 payment terms, there is always a structural gap between revenue earned and revenue received. That gap, measured in weeks or months, is the root cause of most cash flow issues in otherwise healthy businesses.

This distinction matters because most conventional advice about cash flow issues focuses on symptoms: late-paying clients, poor forecasting, and overspending. These are real problems, but they are downstream of the underlying mechanism. Understanding the profit-cash gap is the starting point for fixing it.

The Profit-Cash Gap: How Accrual Accounting Creates the Problem

Accrual accounting is the structural cause of most cash flow problems in profitable service businesses. When revenue is recorded before cash arrives, a permanent timing mismatch opens between the P&L and the bank account. Understanding this mechanism is the first step toward fixing cash flow issues at their source, not just managing the symptoms. (For a deeper look at how CEOs process these financial signals, see Money Psychology for CEOs.)

Most businesses above a certain size are required to use accrual-basis accounting. Under accrual accounting, revenue is recognized when it is earned, not when it is received. The moment you deliver a project and send an invoice, that revenue appears on your P&L. It is “real” revenue by every accounting standard (see Investopedia’s primer on accrual accounting for the technical definition).

But the cash from that invoice has not yet reached your account.

Your rent, on the other hand, is due on the first of the month. Your payroll runs every two weeks. Your software subscriptions are billed automatically. These expenses operate on a cash basis: they leave your account when they are due.

The result is a permanent structural mismatch between revenue recognized and cash received. Revenue is recognized on an accrual basis; expenses are paid on a cash basis. The gap between those two clocks is exactly what creates cash flow issues in profitable businesses.

How Accrual Accounting Creates Cash Flow Issues

Under accrual accounting, revenue is recorded when work is delivered, not when payment arrives. A service business that invoices $50,000 on March 1 with Net-60 terms will not receive that cash until May 1. Payroll, rent, and supplier costs continue through March and April. This two-month gap between recognizing revenue and receiving cash is the structural cause of cash flow problems in profitable service businesses.

Julia Delin frames it directly: “You look at your P&L and everything looks fine. You’re making money. But your bank account is empty because the money you’ve made hasn’t arrived yet.”

For service businesses, the payment timing gap is baked into industry norms. Net-30 is considered fast. Net-60 is standard in many professional services verticals. Net-90 appears in enterprise contracts. That is not a sign of a failing business. That is how service businesses work.

Warning Signs Your Business Has Cash Flow Issues

Six warning signs indicate that cash flow problems are developing before they become a crisis. Catching these signals early is the difference between a manageable timing problem and an emergency credit draw.

The CEOs who catch this pattern early share one habit: they review their accounts receivable aging report weekly, not monthly. By the time a cash shortage becomes apparent in the bank balance, the window for an easy correction has already closed.

These signals tend to appear months before a cash shortage becomes a crisis. A 2019 QuickBooks survey of more than 3,000 small business owners across 10 countries found that 61 percent regularly struggle with cash flow problems even during periods of strong sales performance (QuickBooks State of Small Business Cash Flow, quickbooks.intuit.com). In most cases, the root cause was timing, not profitability.

A strong P&L that does not match your bank balance. If your income statement shows consistent profit but your bank account feels uncomfortably thin, you are likely experiencing the profit-cash gap. How to spot it: Pull your accounts receivable aging report. Add up all invoices outstanding for more than 30 days. If that total exceeds one month of operating expenses, the profit-cash gap is actively working against your business.

Paying suppliers before clients have paid you. If you are regularly covering costs for work that has not yet been paid by the client, your cash conversion cycle is working against you. The gap between cash going out and cash coming in is the core problem.

Accounts receivable aging beyond 45 days. Most service businesses set Net-30 terms. When invoices regularly stretch past 45 days without payment, receivables are building faster than cash is arriving. How to spot it: Sort your AR aging report into 0-30, 31-45, and 46+ day buckets. If more than 20 percent of outstanding receivables fall in the 46+ bucket, your collection process needs immediate attention.

Using a credit line to cover payroll during profitable months. This is a critical signal. If a month shows solid revenue but you are drawing on a line of credit to make payroll, cash is not arriving fast enough to match when it is needed.

Revenue growth that tightens your cash position. This counterintuitive pattern, sometimes called the growth trap, is one of the most common cash flow issues for scaling companies. It happens when a business lands larger contracts and extends more credit in the process. (See also: How to Scale a B2B Startup for the broader scaling challenges that amplify this problem.) More revenue on the P&L, more outstanding receivables, less available cash. A marketing agency growing from $500,000 to $1.2 million in annual revenue may simultaneously watch its available cash shrink, because larger clients typically demand longer payment terms. The business is growing; the bank account is not keeping up. How to spot it: Compare monthly revenue recognized against cash actually received over the past six months. If recognized revenue is growing but cash received is not tracking proportionally, the growth trap is active.

Seasonal revenue gaps. If your business follows seasonal patterns, the low-billing months can deplete reserves built during peak periods faster than expected. The warning sign is not the slow month itself but the absence of a cash buffer that can cover fixed costs, primarily payroll and rent, through the trough. Service businesses with seasonal clients, including event companies, landscaping firms, and retail support agencies, face this pattern every year.

None of these six warning signals means a business is failing. They mean the payment timing structure needs attention before it becomes a crisis.

Why Are Service Businesses More Vulnerable to Cash Flow Issues?

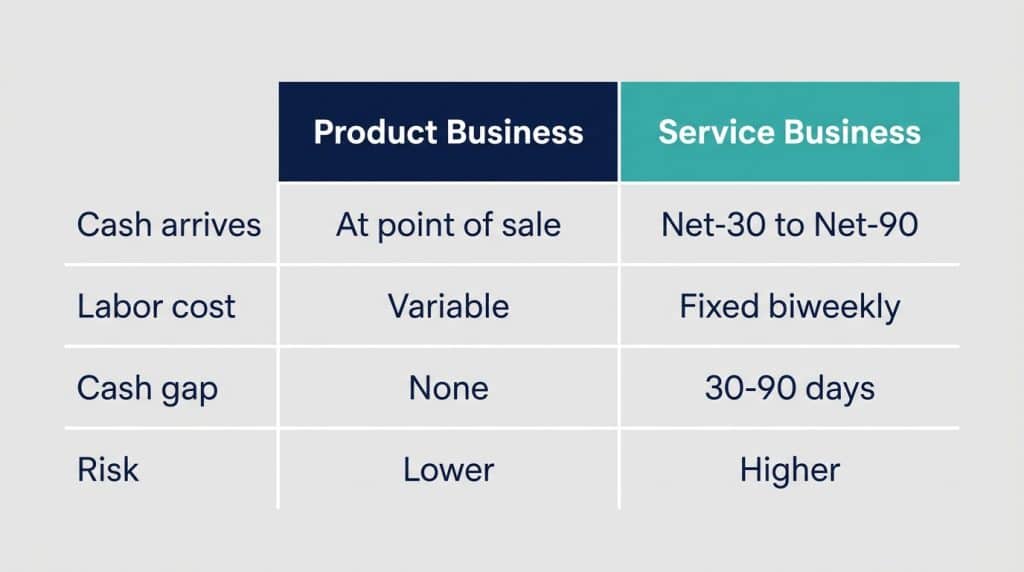

Service businesses face more severe cash flow problems than product businesses because of one structural condition: labor is paid immediately, while client payments arrive 30 to 90 days later.

The most vulnerable service businesses share a single characteristic: the business owner monitors the P&L closely but rarely checks the accounts receivable aging report. By the time the bank balance signals a problem, the accounts receivable have been quietly building for months.

Not all businesses experience cash flow issues equally. Service businesses, including consulting firms, staffing agencies, marketing agencies, cleaning companies, and IT service providers, face structural conditions that make the profit-cash gap especially acute.

The data supports this. The Federal Reserve’s 2024 Small Business Credit Survey found that cash flow management was the most frequently cited financial challenge among service sector employers, ranking above concerns about rising costs, revenue growth, or hiring (Federal Reserve, federalreserve.gov). Service businesses are not simply more anxious about cash. They face a structural timing problem that other sectors largely avoid.

Payment terms are an industry norm, not a negotiation. In many service verticals, Net-30 or Net-60 terms are simply how business is done. Enterprise clients often demand Net-90. Refusing these terms may result in the loss of the contract.

There is no inventory to liquidate. A product business facing a cash crunch can sell down inventory to generate immediate cash. A service business has no equivalent. The product was delivered; the cash is tied up in a receivable.

Labor costs are immediate; revenue is deferred. The highest cost in most service businesses is people. Payroll runs on a fixed schedule, weekly or biweekly, regardless of when clients pay. A staffing agency might pay its workers on Friday for work completed Monday through Friday, then wait 45 days for the client invoice to clear.

Client concentration amplifies risk. When one or two clients represent 40 to 60 percent of revenue, their payment timing governs the entire business’s cash position. A single slow-paying anchor client, even a perfectly good client, can destabilize the business.

The Service Business Cash Flow Paradox

Service businesses face a structural cash-flow challenge that product businesses largely avoid: labor is the primary cost, and it is paid immediately. Revenue, collected through invoiced client payments, arrives 30 to 90 days later. The gap between paying people and getting paid for their work is not a management failure. It is a structural feature of how service businesses operate.

Julia Delin makes the same point directly: the payment gap is not something service business owners created through poor management. It is built into the industry’s structure.

Dynamic Discounting: The Tool Enterprise Has Used for Decades

Dynamic discounting converts a future receivable into immediate cash for a 1 to 3 percent discount.

The payment gap is a solved problem at the enterprise level. Most small business owners have simply never had access to the solution.

The mechanism is called dynamic discounting. Here is how it works: instead of waiting 30, 60, or 90 days for an invoice to be paid at full value, the vendor, meaning the service provider, offers a small discount, typically 1 to 3 percent, in exchange for immediate payment. The buyer pays today and receives a discount. The seller receives cash today instead of waiting weeks or months.

Dynamic discounting is not a new concept. Enterprise accounts payable departments have used dynamic discounting for decades. Companies like SAP, through its acquisition of Taulia, a deal valued at less than $1 billion, built sophisticated platforms that processed enormous volumes of AP transactions this way.

According to Julia Delin, the total volume of US accounts payable runs into the trillions annually. Enterprises use dynamic discounting to put that capital to work: buyers earn an effective return by paying early and capturing the discount; sellers receive cash now rather than later.

Direct Answer Block: What Is Dynamic Discounting?

Dynamic discounting is a payment mechanism in which a vendor offers a buyer a small percentage discount, typically 1 to 3 percent, in exchange for immediate payment rather than standard Net-30 or Net-60 terms. For the buyer, early payment at a discount yields an effective annual return that often exceeds that of short-term investment alternatives. For the seller, it converts a future receivable into present cash. Enterprise companies have used dynamic discounting at scale for decades.

The barrier to dynamic discounting, until recently, was access. The platforms that enabled dynamic discounting at scale, including Taulia and C2FO, were built for Fortune 500 procurement departments. A cleaning company or a marketing agency could not plug in.

That is what Cheque is building: dynamic discounting infrastructure sized for small service businesses. The mechanism is the same. The interface is designed for a business owner who needs cash now, not a Fortune 500 AP team.

How to Fix Cash Flow Issues: From Band-Aids to Systemic Solutions

Fix cash flow issues at three levels: tactical, structural, and systemic. Tactical fixes reduce the lag. Structural fixes improve visibility. Systemic fixes close the gap permanently by converting future receivables into present cash.

The service business owners who solve cash flow issues permanently stop treating early payment discounts as a crisis tool and start offering them as a standing policy. That shift, from reactive to structural, is what separates businesses that manage the cash gap from those that eliminate it.

Short-term tactics.

Invoice immediately after project delivery. Follow up on overdue invoices without delay. A week of silence on a late invoice quickly becomes a month. Shorten payment terms where the client relationship allows, Net-15 instead of Net-30, and the effect compounds over a full year.

Process improvements.

Build a 13-week cash flow forecast. Knowing when cash will arrive, not just whether you are profitable, allows you to plan payroll and supplier payments around real cash timing. Separate cash thinking from P&L thinking: review your bank balance alongside your income statement. Build a cash reserve. Three months of operating expenses as a buffer do not solve the structural gap, but they make the gap survivable. For the foundational financial skills behind these disciplines, see Financial Acumen for CEOs.

Not all fixes carry equal weight. This comparison shows where each approach sits on the spectrum from symptom relief to root cause resolution:

| Fix | Time to impact | Addresses root cause? | Scalability |

|---|---|---|---|

| Invoice faster | Immediate | Partial | High |

| Shorten payment terms | 30-60 days | Partial | Medium |

| Follow up on late invoices | 1-2 weeks | No | Low |

| 13-week cash flow forecast | Ongoing | No | High |

| Cash reserve (3 months operating) | Months to build | No | Medium |

| Early payment discount (standing policy) | Immediate | Yes | High |

| Dynamic discounting | Immediate | Yes | High |

The two bottom rows are the only approaches that convert future receivables into present cash without adding debt. Everything above them manages the gap without closing it.

The systemic layer: early payment discounts and dynamic discounting.

Early payment discounts are underused. Instead of chasing clients to pay on time, you offer a small financial incentive for paying early, typically 1 to 2 percent off the invoice in exchange for payment within 10 days.

Most business owners who have tried this did so reactively: a one-time offer to a single client during a cash crunch. That is not a system. Dynamic discounting, as Julia Delin describes it, is a standing, structural offering. Clients who want the discount can always take it. The seller maintains a more consistent cash flow. The buyer gets a return on early payment that typically exceeds money market rates.

That standing-policy approach is the enterprise model brought to small businesses. The band-aids address symptoms. Dynamic discounting addresses the gap.

FAQ

What are cash flow issues?

Cash flow issues occur when a business lacks sufficient cash to meet its financial obligations, including payroll, rent, and supplier payments, regardless of its profitability. The most common form in service businesses is a timing gap: revenue is earned when work is delivered, but cash does not arrive until clients pay, which can take 30 to 90 days.

What is the difference between cash flow and profit?

Profit measures whether revenue exceeds expenses over a period, calculated using accrual accounting, which records revenue when earned rather than when received. Cash flow reflects what is actually in the bank at any given moment. A business can be highly profitable, with strong margins and growing revenue, and still run out of cash if clients pay slowly and operating costs are due immediately.

What are the warning signs of poor cash flow?

Key warning signs include a consistently strong P&L that does not match your bank balance; accounts receivable regularly aging past 45 days; using a credit line to fund payroll during profitable months; paying suppliers before clients have paid you; and revenue growth that somehow leaves less cash available rather than more. These signals point to a timing problem, not a profitability problem.

How do you fix cash flow issues in a service business?

Fix cash flow issues at three levels. Tactically: invoice faster, follow up immediately on late payments, and shorten payment terms where possible. Structurally: build a 13-week cash flow forecast, maintain a cash reserve covering three months of operating expenses, and track bank balance separately from P&L. Systemically: implement early payment discounts or dynamic discounting as a standing policy, converting future receivables into present cash without relying on debt.

What is dynamic discounting?

Dynamic discounting is a payment mechanism in which a vendor offers a buyer a small percentage discount, typically 1 to 3 percent, in exchange for paying an invoice immediately rather than waiting for standard payment terms to expire. For the buyer, it generates an effective return on early payment. For the seller, it converts a future receivable into immediate cash. Enterprise companies have used dynamic discounting for decades; it is now becoming accessible to small service businesses.

What is an early payment discount?

An early payment discount is a pricing incentive a vendor offers to encourage faster payment. For example, terms written as “2/10 Net 30” mean the buyer receives a 2 percent discount if they pay within 10 days instead of the standard 30. Used reactively, early payment discounts are a one-time tool for cash crunches. Used systematically as a standing policy offered to all clients, they function as a continuous mechanism for converting receivables into cash.

What are the common challenges in cash flow management?

The most common challenges are: confusing profit with cash availability, because a profitable business can be cash-poor; payment timing mismatches, where client payments arrive later than operating costs come due; accounts receivable aging, where invoices accumulate faster than they are collected; seasonal revenue fluctuations without adequate reserves to cover slower periods; and rapid growth that extends more credit than the business can float while waiting for payment.

Conclusion

Cash flow issues are not a sign that a business is failing. They are a structural feature of how service businesses work, and once you understand that, the path forward becomes clearer.

The profit-cash gap exists because accounting records revenue before cash arrives, widens under standard Net-30 to Net-90 payment terms, and hits service businesses hardest, where labor costs are immediate.

Julia Delin’s insight is worth holding: the tools that solved this problem at the enterprise level, dynamic discounting infrastructure that processed trillions in AP, were never designed for the cleaning company, the staffing agency, or the consulting firm. That gap in access is starting to change.

In the meantime, the fundamentals matter. Invoice faster. Forecast in cash terms, not just P&L terms. Build reserves. Offer early payment discounts as a standing policy rather than a crisis measure.

Cash flow issues are manageable. It starts with recognizing that profit and cash are two different numbers, and planning for both.

Some topics we explore in this episode include:

Listen to the episode

Subscribe to & Review the Predictable B2B Success Podcast

Thanks for tuning into this week’s Predictable B2B Podcast episode! If the information from our interviews has helped your business journey, please visit Apple Podcasts, subscribe to the show, and leave us an honest review.

Your reviews and feedback will not only help me continue to deliver great, helpful content but also help me reach even more amazing founders and executives like you!

Related Links

Guest resources:

– Julia Delin on LinkedIn: linkedin.com/in/juliadelin

– Cheque (fintech): chequepay.co

Related Resources

Related Sproutworth episodes:

– How to Scale a B2B Startup: Lessons From 500 CEO Interviews

– Money Psychology for CEOs: Why Data-Driven Leaders Still Make Emotional Decisions

– Financial Acumen: How to Master Financial Strategy and Align With Core Values