Table of Contents

You’re 60 days from closing your Series A. Your term sheet is signed. Due diligence begins. Then your lawyer mentions you never filed 83(b) elections.

Your raise just got complicated.

Most founders believe they understand what investors want during due diligence. They’re wrong. After analyzing hundreds of funded B2B tech startups from seed to Series C, one pattern emerges: the legal mistakes startups make during fundraising aren’t the ones founders expect. While CEOs obsess over pitch decks and financial projections, VCs are quietly walking away because of preventable legal errors, missing 83(b) elections, unassigned IP, wrong corporate structure, lack of founder vesting, and other issues discovered during investor due diligence.

The data is sobering. While only 2% of startup failures cite legal issues as the primary cause, a 2024 DesignRush study finds that an additional 2% encounter legal complications, including IP disputes, unclear founder agreements, or regulatory missteps that stall growth. But here’s what those statistics miss: these legal mistakes startups make don’t just kill startups outright. They kill deals.

This isn’t another generic legal checklist. This is the investor playbook for what actually kills rounds, how much it costs to fix, and what you need to triage first.

📊 KEY STATISTIC

According to Failory’s 2024 startup failure analysis, 18% of startups face regulatory and legal challenges that contribute to closure. However, Legal Nodes’ research from their due diligence study shows that 65% of startup failures stem from founder conflicts – often triggered by a lack of vesting agreements or unclear equity splits discovered during fundraising.

About Jeff Holman

Jeff Holman is the founder of Intellectual Strategies, a fractional legal services firm that’s redefining how startups and scaling businesses access legal support. With degrees in electrical engineering and law, and an MBA, Jeff brings a unique, multidisciplinary perspective to legal strategy.

His background includes extensive patent work with companies ranging from IBM and Intel to garage startups, and a pivotal transition from traditional law firm practice to in-house counsel that revealed a fundamental disconnect between how attorneys bill and what businesses actually need. Today, he leads the first fractional legal team model, providing companies with expert legal advice at key growth points without the full-time overhead.

Expert Insight: Jeff Holman, Founder of Intellectual Strategies

“Document stuff. It sounds simplistic, but it’s the legal advice most startups ignore until it’s too late. The absence of documentation doesn’t mean you’ve done something wrong – it means investors can’t verify you’ve done things right. In their risk calculation, that’s the same thing.”

“IBM’s patent licensing was their number one revenue stream at one point, larger than any hardware or software business. IP isn’t just legal protection – it’s enterprise value. Investors know this.”

“Startups don’t need attorneys on retainer. They need strategic legal guidance at specific inflection points: incorporation, first hires, first funding, major contracts, and subsequent funding rounds.”

The Triage Framework: What Kills Deals vs What Slows Them

Here’s the uncomfortable truth: founders treat legal documentation as a checkbox. Investors treat it as a dealbreaker.

But not all legal mistakes startups make are equal. Understanding the difference between red flags (deal killers) and yellow flags (deal slowers) determines whether you close or watch your round collapse.

Red Flag vs Yellow Flag Comparison

| Factor | Red Flags (Deal Killers) | Yellow Flags (Deal Slowers) |

|---|---|---|

| Impact | 60-90% of deals die | 30-60 day delays |

| Examples | Missing IP, Dead equity, Wrong structure | Cap table errors, Misclassification |

| Fix Cost | $50K-$200K+ | $10K-$50K |

| Fix Timeline | 60-120 days (if possible) | 30-60 days |

| Investor Response | Walk away or massive valuation cut | Delay close, minor valuation impact |

| Can Kill Deal? | Yes (60-90% of cases) | Rarely (5-10% of cases) |

Red Flags (Deal Killers):

- Missing IP assignments from core team members

- No founder vesting or departed founder holding 40% equity

- Wrong corporate structure (LLC or S-Corp seeking VC funding)

- Unissued or incorrectly issued founder stock

- Active lawsuits or regulatory violations

Yellow Flags (Deal Slowers – Fixable in 30-90 days):

- Cap table errors or missing documentation

- Employee misclassification issues

- Missing board minutes from the past 12 months

- Incomplete employment agreements

- Privacy policy gaps

When I work with Series B SaaS founders on educational email courses on fundraising preparation, the same blind spot rears its head. They’ll spend 40 hours perfecting financial models but allocate zero hours to documenting IP assignments from contractors hired two years ago.

VCs think differently. They’re not just evaluating your product. They’re assessing legal risk that could evaporate their entire investment.

According to Legal Nodes’ 2025 investor due diligence analysis, around 65% of startups fail due to founders’ conflicts. Yet most early founder agreements are verbal. When investor due diligence begins and this surfaces, the deal stalls. Best case: expensive emergency legal work ($15,000-$50,000). Worst case: the investor walks.

The pattern repeats across every funding stage. A Series A cleantech company I recently worked with had exceptional unit economics and a clear path to profitability. Their round fell apart during due diligence when investors discovered their core IP was created by an employee who hadn’t signed assignment agreements.

The round didn’t just delay. It died.

Common Legal Mistakes Startups Make: Cost & Timeline Overview

| Legal Mistake | Deal Impact | Fix Cost | Fix Timeline | Fixable? |

|---|---|---|---|---|

| Wrong Corp Structure (LLC/S-Corp) | Red Flag | $50K-$200K | 30-90 days | Sometimes |

| Missing 83(b) Elections | Yellow Flag | $0-$500K (tax) | Unfixable after 30 days | No |

| Missing IP Assignments | Red Flag | $10K-$100K | 30-120 days | Sometimes |

| No Founder Vesting | Red Flag | $5K-$30K | 30-90 days | Yes (painful) |

| Cap Table in Excel | Yellow Flag | $3K-$15K | 14-45 days | Yes |

| Employee Misclassification | Yellow Flag | $25K-$200K | 60-180 days | Yes |

| Privacy Compliance Gaps | Yellow-Red | $15K-$75K | 45-120 days | Yes |

| Stock Not Formally Issued | Red Flag | $10K-$100K | 30-90 days | Yes (expensive) |

| Wrong Type of Lawyer | Yellow-Red | $20K-$100K | 30-120 days | Yes |

| Exclusive Agreements | Red-Yellow | $5K-$30K | 30-180 days | Sometimes |

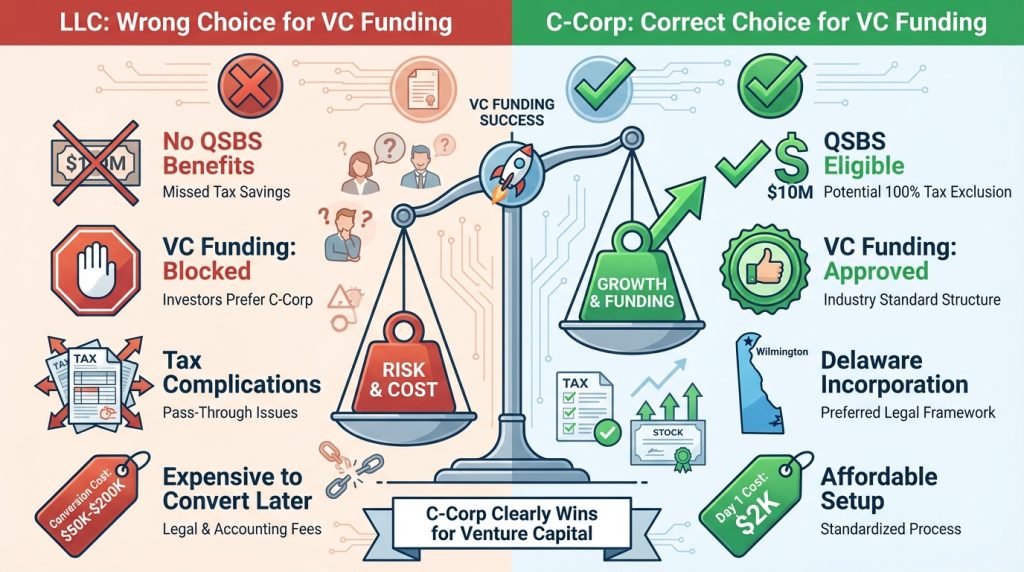

Mistake #1: Wrong Corporate Structure (C-Corp or Nothing)

QUICK ANSWER: If you’re an LLC or S-Corp seeking venture capital, your raise is already over. VCs won’t even start diligence. Only Delaware C-Corps qualify for QSBS (Qualified Small Business Stock) treatment, which allows investors to exclude up to $10 million from capital gains tax. Converting from LLC/S-Corp after issuing equity creates $50,000-$500,000+ tax liabilities and prevents existing equity from qualifying for QSBS benefits. Cost to fix: $50K-$200K. Timeline: 30-90 days if even possible.

Deal Impact: Red flag. Kills 90% of VC deals immediately.

Fix Cost: $5,000-$25,000 in legal fees + potential $50,000-$500,000 in tax liability

Fix Timeline: 30-90 days (if even possible)

If you’re an LLC or S-Corp seeking venture capital, your raise is already over. VCs won’t even start diligence.

Here’s why: Qualified Small Business Stock (QSBS) exemption allows investors, founders, and early employees to potentially exclude up to $10 million (or 10x their investment, whichever is greater) from federal capital gains tax when selling their shares. But QSBS only applies to C-Corps.

Converting from LLC or S-Corp to C-Corp after you’ve issued equity creates two catastrophic problems:

Problem 1: Existing equity doesn’t qualify for QSBS treatment. Your investors lose millions in tax benefits.

Problem 2: The conversion itself triggers taxable events. Founders can face six-figure tax bills on paper gains.

A Series B company I partnered with incorporated as an LLC “for flexibility.” When they attempted to convert 18 months later during fundraising, tax complications reduced their valuation by 15%. Investors demanded that founder equity be restructured. Two founders quit over the dispute.

Key Legal Concepts Explained

QSBS (Qualified Small Business Stock) is related to C-Corp structure because only C-Corp stock qualifies for the $10M capital gains exclusion. This matters for investor due diligence because VCs expect QSBS eligibility.

C-Corp structure must exist at incorporation – converting later from LLC or S-Corp means existing equity won’t qualify for QSBS benefits even after conversion, making your company unfundable by venture capitalists.

Should You Convert From LLC to C-Corp?

Decision Tree:

- Are you raising venture capital?

- Yes → Convert to C-Corp immediately

- No → LLC may be fine for now

- Have you already issued equity?

- Yes → Conversion triggers tax events ($50K-$500K potential liability)

- No → Convert before issuing (clean, no tax impact)

- Do you have investors or plan to within 12 months?

- Yes → C-Corp required for QSBS ($10M tax exclusion)

- No → Can delay, but convert before first funding

- Can you afford $5K-$25K conversion cost?

- Yes → Start conversion process (30-90 days)

- No → Use legal tech platforms (Carta Launch, Clerky: $1K-$5K)

Bottom line: If you’re raising VC money ever, be C-Corp from day one.

Cost Impact: With vs Without Proper Structure

Scenario A: Wrong Structure (LLC → C-Corp)

- Incorporation cost: $500 (LLC)

- Conversion cost 18 months later: $25,000

- Tax liability from conversion: $150,000

- Delayed fundraise: 90 days

- Reduced valuation: -15% ($750K loss on $5M round)

- Total cost: $925,000+

Scenario B: Right Structure (C-Corp from Day 1)

- Incorporation cost: $2,000 (C-Corp)

- Conversion cost: $0

- Tax liability: $0

- Fundraise delay: 0 days

- Valuation impact: $0

- Total cost: $2,000

Savings from doing it right: $923,000

Action Plan (If You’re Already Wrong)

Week 1-7: Immediate Assessment

- [ ] Consult with startup-focused tax attorney (Orrick, Cooley, Wilson Sonsini level, not your uncle’s lawyer)

- [ ] List all current equity holders (founders, employees, advisors)

- [ ] Gather all equity issuance documents

Week 2-4: Tax Impact Analysis

- [ ] Model tax implications of conversion for all stakeholders

- [ ] Calculate QSBS benefits lost from existing equity

- [ ] Determine if conversion is worth it vs staying LLC and pivoting away from VC funding

Week 4-6: Conversion Execution (If Proceeding)

- [ ] File all required state and federal forms for conversion

- [ ] Notify all equity holders of tax implications

- [ ] Update operating agreement to C-Corp bylaws

Week 6-8: Cap Table Restructure

- [ ] Restructure cap table to reflect C-Corp equity

- [ ] Issue new stock certificates

- [ ] Update Delaware (or relevant state) filings

Week 8-12: Post-Conversion Cleanup

- [ ] Obtain new 409A valuation post-conversion

- [ ] Update all equity agreements

- [ ] Prepare legal opinion letter for investors explaining conversion

Cost: $50,000-$200,000 (legal + tax + potential tax liability)

Prevention Plan (If Starting Fresh)

Day 1 Checklist:

- [ ] Incorporate as Delaware C-Corp (cost: $1,500-$2,500)

- [ ] File 83(b) elections for all founders (cost: $0-$500)

- [ ] Set up professional cap table software (Carta, Pulley: $2,000-$10,000/year)

- [ ] Implement 4-year vesting with 1-year cliff for all founders

Cost: $4,000-$13,000 upfront Savings vs fixing later: $900,000+

When developing content strategies for funded startups, this pattern often appears: founders optimize for today’s simplicity rather than tomorrow’s scalability. C-Corp structure isn’t overhead. It’s the foundation investors require.

Mistake #2: Missing 83(b) Elections (The 30-Day Tax Bomb)

QUICK ANSWER: An 83(b) election is a tax form that must be filed within 30 days of receiving vesting stock. Missing this deadline creates tax liabilities of $50,000-$500,000+ on “phantom income” as shares vest. This mistake cannot be fixed after 30 days and is discovered during due diligence when investors calculate founder tax obligations that could force share sales. Cost: Unfixable. The IRS has a hard 30-day deadline with no exceptions.

Deal Impact: Yellow flag. Delays close 30-60 days, reducing valuation by 5-15%

Fix Cost: Unfixable. You owe the IRS what you owe. Often $50,000-$500,000+

Fix Timeline: Too late if you missed the 30-day window

Here’s the nightmare scenario: You receive vesting stock. You don’t file an 83(b) election within 30 days. Your company grows from a $2M valuation to $20M over four years. As shares vest monthly, you owe income tax on the current value of each vesting tranche.

You now owe taxes on $500,000 of “income” from vesting shares. You haven’t sold anything. You have no cash. The IRS doesn’t care.

This is called phantom income. It destroys founders.

According to multiple startup legal analyses from SPZ Legal (April 2025) and other top startup law firms, failing to file 83(b) elections is one of the most expensive startup legal mistakes because it’s irreversible. The IRS gives you exactly 30 days from receiving vesting stock. Miss it by one day? You’re paying tax on every vesting event at the current valuation instead of at the (much lower) strike price.

Key Legal Concepts Explained

83(b) Election is a tax filing related to founder vesting because it determines when you pay taxes on vesting stock. Without 83(b), you pay tax each time shares vest (expensive). With 83(b), you pay once at grant (cheap).

Phantom income is the tax consequence of missing 83(b) elections where founders owe income tax on vesting shares based on current valuation, despite having no cash from selling shares.

What Actually Happens: With vs Without 83(b)

Without 83(b): • You get 4-year vesting with 1-year cliff • Company value increases from $1M to $10M • Every month shares vest, you owe tax on that month’s valuation • Over 4 years, you could owe $200,000+ in taxes on shares worth $400,000

With 83(b) (filed within 30 days): • You pay tax once on the initial low valuation (often $0-$500) • All future vesting events are tax-free • When you sell shares, you pay capital gains (not income tax) on appreciation

Investors discover missing 83(b) elections during diligence. They immediately calculate: “This founder owes $300K in taxes they can’t pay. They’ll have to sell shares to cover it. That dilutes everyone and signals poor planning.”

People Also Ask: 83(b) Elections

Can I file 83(b) after 30 days? No. The IRS has a hard 30-day deadline from the date you receive vesting stock. No exceptions, no extensions, no fixing it later. If you miss it, you will owe income tax on every vesting event based on the company’s current valuation.

What happens if I don’t file 83(b)? You’ll owe income tax every time shares vest, based on current valuation. For a company growing from $2M to $20M, this creates $50K-$500K+ tax liability on “phantom income” you haven’t actually received as cash. You’ll need to pay these taxes out of pocket or sell shares to cover them.

Do investors check 83(b) filings? Yes, always. It’s standard in legal due diligence checklists. Missing 83(b) elections signal poor tax planning and create concerns that founders will need to sell shares to pay taxes, diluting everyone. This can delay funding by 30-60 days and reduce valuations by 5-15%.

How much does 83(b) cost to file? $0-$500. The form itself is free (1 page from IRS.gov). Many startup attorneys include it in formation packages. The cost of NOT filing is $50K-$500K+ in unnecessary taxes over 4 years of vesting.

When exactly do I need to file 83(b)? Within 30 days of the date you receive restricted stock or exercise stock options that are subject to vesting. The 30-day clock starts when you sign the stock purchase agreement, not when the company incorporates or when vesting begins.

83(b) Election Filing Checklist

Days 1-7 (After Receiving Vesting Stock):

- [ ] Obtain 83(b) election form from attorney or download from IRS.gov

- [ ] Fill out with: Your name, SSN, number of shares, price paid per share, fair market value

- [ ] Make 3 copies (one for IRS, one for company, one for your records)

- [ ] Sign and date all copies

Days 7-14:

- [ ] Send original to IRS via certified mail with return receipt requested

- [ ] Keep tracking number and certified mail receipt

- [ ] Send copy to company for corporate records

- [ ] File copy in your personal tax records

Days 14-30:

- [ ] Verify IRS received filing (check certified mail tracking)

- [ ] Confirm company received and filed their copy

- [ ] Save all receipts and documentation

- [ ] Attach copy to your next federal tax return

Cost: $0-$50 (certified mail fees) Time: 2 hours total Consequence of missing: $50,000-$500,000+ tax liability over vesting period

Action Plan (Prevention Only – This Cannot Be Fixed After 30 Days)

Day 1: Receive vesting stock

Day 1-7: Have startup attorney prepare 83(b) election form (1 page)

Day 7-14: File with IRS via certified mail, keep receipt

Day 14-21: Send copy to company for records

Day 21-30: Verify IRS received (check certified mail tracking)

If You Already Missed It

Be honest with investors during diligence. Calculate total tax liability. Show you have plan to cover it (personal funds, bonus structure, etc.). Some investors will walk. Others will restructure to account for it.

A pattern I notice across funded B2B tech companies: the best teams file 83(b) elections before anyone asks. They understand tax planning isn’t about compliance. It’s about preserving founder equity through growth.

Mistake #3: IP Ownership That’s “Probably Fine”

QUICK ANSWER: Without signed IP assignment agreements from every person who touched your product, you don’t legally own your technology. During due diligence, investors verify IP ownership and walk away if assignments are missing. Common gaps: contractors without work-for-hire agreements, founders who developed IP while employed elsewhere, offshore developers never signed assignments. Cost to fix: $10K-$100K if fixable. Timeline: 30-120 days. Many cases unfixable if people refuse to sign or can’t be located.

Deal Impact: Red flag. Kills 60% of deals where it appears.

Fix Cost: $10,000-$100,000 (if fixable); company death if unfixable

Fix Timeline: 30-120 days (if parties cooperate)

If you’re not certain who owns your intellectual property, investors are certain they’re not funding you.

IP ownership disputes rank among the top reasons venture-backed deals collapse during due diligence. According to Failory’s 2024 analysis, while legal issues account for a small share of overall failures, regulatory and legal challenges account for 18% of startup closures.

The problem isn’t usually dramatic. It’s bureaucratic:

- Founder develops initial code while employed elsewhere (employer may own it)

- Contractor builds critical feature without work-for-hire agreement

- Early team members leave before signing IP transfer documents

- Offshore developers never signed IP assignments

- Co-founder works on product during grad school (university may own IP)

Each scenario creates a potential claim against your company’s core assets. Investors won’t fund potential claims.

Key Legal Concepts Explained

IP assignment agreements transfer intellectual property ownership from creators (employees, contractors, founders) to the company. Without signed agreements, individuals retain ownership of code, designs, and inventions they created – even if they were paid to create them.

Work-for-hire clauses in contractor agreements specify that the company owns all IP created by contractors. Standard contractor agreements often lack these clauses, meaning contractors retain IP ownership by default.

Real Cost Example: IP Dispute That Killed a Series A

A SaaS company raised $2M seed round. During Series A diligence, investors discovered their core algorithm was created by a founder while employed at Google. Google’s standard employment agreement claimed ownership of all inventions during employment.

Options:

- Negotiate with Google: $50,000 in legal fees, 6-month delay, gave Google 5% equity

- Rewrite algorithm: $200,000 in development costs, 8-month delay, lost customer momentum

- Walk away: What they did. Series A died.

Outcome: Company shut down 14 months later without funding.

When ghostwriting LinkedIn content for B2B tech executives, I emphasize this constantly: every piece of code, every design asset, and every proprietary content asset requires documented ownership. The executive who says “our contractor would never claim ownership” is the same one who, during diligence, learns that legal rights are not bound by assumed intentions.

What Investors Actually Verify

☑ IP assignment agreements signed by every person who touched the product

☑ Work-for-hire clauses in all contractor agreements

☑ Verification no team members were bound by prior employment IP clauses

☑ All pre-incorporation work formally assigned to company

☑ Patent applications filed where applicable

☑ Trademark registrations for brand/name

IP Ownership Audit Checklist

Week 1-2: Complete IP Audit

- [ ] List every person who created IP (code, design, content, inventions)

- [ ] Create spreadsheet: Name, Role, Dates Active, IP Created, Agreement Status

- [ ] Identify: Founders, employees, contractors, advisors, interns, offshore developers

- [ ] Note: Pre-incorporation work, work done while employed elsewhere

Week 3-4: Contact Everyone Missing IP Assignments

- [ ] Send standardized IP assignment agreement (get template from startup attorney)

- [ ] For current team: Make signing condition of continued employment

- [ ] For departed employees: Offer small equity consideration ($500-$5,000) to sign

- [ ] For contractors: May need to pay additional fee or small equity grant

- [ ] Document all attempts with emails, certified letters

Week 4-8: Handle Problem Cases

- [ ] Offshore contractors: May need to negotiate payment or equity ($1,000-$10,000)

- [ ] Former employers: Need legal review of employment agreements

- [ ] Unreachable people: Hire skip tracer, document exhaustive attempts

- [ ] People who refuse: Get legal opinion on risk, consider design-around

Week 8-12: Clean Documentation Package

- [ ] Signed IP assignments from 100% of contributors

- [ ] Legal opinion letter for any gaps explaining risk

- [ ] Alternative solutions for unfixable gaps (rewrite code, design-around patents)

- [ ] Timeline for completing any outstanding work

Cost: $10,000-$100,000, depending on the number of contributors and cooperation

Timeline: 30-120 days minimum

Prevention Plan: Day One IP Protection

Before Anyone Writes Code:

- [ ] Founder IP assignments signed at incorporation

- [ ] Employee offer letters include IP assignment clause

- [ ] Contractor agreements include work-for-hire provision

- [ ] Consultant/advisor agreements include IP transfer

- [ ] Intern agreements include IP assignment

Use templated agreements from startup law firms:

- Orrick, Cooley, Wilson Sonsini provide standard IP assignment templates

- Carta Launch, Clerky, Capbase include IP agreements in formation packages

- Cost: $1,000-$3,000 for complete template package

Ongoing maintenance:

- Review IP assignments quarterly

- Update the list of contributors monthly

- Get signatures before people depart

- Keep a centralized file of all signed agreements

Jeff Holman emphasizes that IP strategy isn’t just defensive. It’s a revenue driver. IBM’s patent licensing reportedly was its top revenue stream at one point, larger than any of its hardware or software businesses. While most startups won’t reach that scale, the principle holds: documented, defensible IP creates options.

Investors know this. They’re looking for founders who understand IP isn’t just legal protection. It’s the enterprise value.

💡 CONTRARIAN INSIGHT

Common belief: “Our contractors would never claim ownership of work we paid them to create.”

Reality from 500+ podcast interviews with funded CEOs: Legal ownership follows written agreements, not moral assumptions. In three separate cases, I’ve witnessed contractors claim ownership of critical features during acquisition talks, resulting in $10M-$50M exits. The founders’ response: “But we paid them!” The acquirer’s response: “No signed work-for-hire agreement = we’re out.”

Why this matters: Verbal agreements and good faith mean nothing in legal due diligence. Signed IP assignments are binary: you have them, or you don’t.

Mistake #4: Founder Equity Without Vesting (The Dead Equity Problem)

QUICK ANSWER: Dead equity occurs when departed founders retain significant ownership without contributing. Without vesting agreements, founders who leave after 6 months keep their full equity stake. Investors won’t fund companies where non-contributors own 20-40%. Cost to fix: $5K-$30K in legal fees plus painful founder negotiations. Timeline: 30-90 days if founders cooperate. Implementation requires retroactive vesting where founders credit time already served (e.g., 18 months working = 37.5% vested on 4-year schedule).

Deal Impact: Red flag. Kills 70% of deals where it appears.

Fix Cost: $5,000-$30,000 in legal fees + massive founder relationship damage

Fix Timeline: 30-90 days of painful negotiations

Nothing telegraphs “amateur hour” to VCs faster than discovering founders hold unvested equity or departed founders still own 30-40% of the company.

This is called “dead equity.” A founder no longer contributes but still owns significant shares. According to Frost Brown Todd attorneys’ October 2025 analysis, who’ve worked with countless startups, dead equity is a deal-killing red flag that investors simply won’t accept.

Founder vesting protects everyone:

- Ensures equity aligns with ongoing contribution

- Prevents departing founders from walking away with disproportionate ownership

- Gives remaining team members and investors confidence

- Creates a framework for handling founder departures

Yet according to multiple analyses, founder equity disputes remain a leading cause of startup failure. The reason is simple: equity conversations feel uncomfortable, so founders delay them.

Key Legal Concepts Explained

Dead equity is a consequence of missing founder vesting, in which departing founders retain significant ownership without contributing. This raises red flags for investors who won’t fund companies in which non-contributors own 20-40%.

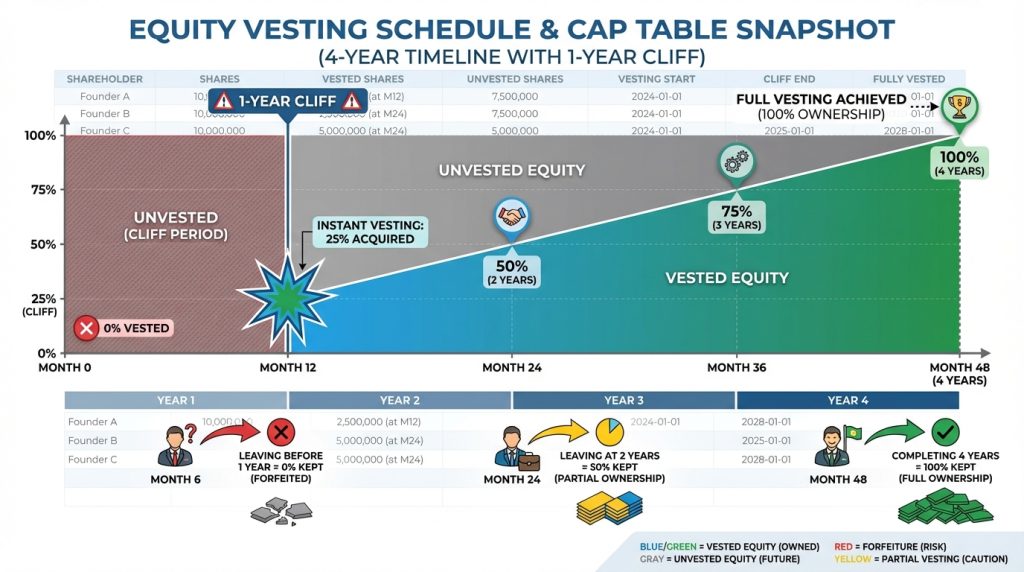

Founder vesting typically follows a 4-year schedule with a 1-year cliff: founders earn 0% equity for the first year, then 25% vests at 12 months (the cliff), and the remaining 75% vests monthly over the next 36 months. If the founder leaves before 1 year, they get nothing. If they leave after 2 years, they keep 50%.

Retroactive vesting solves the problem when implementing vesting after founders have already been working. Founders receive credit for time served (e.g., 18 months working = 37.5% already vested), then continue vesting going forward.

The Dead Equity Nightmare: Real Scenario

Scenario: Three co-founders split equity 33/33/33 with no vesting. After 8 months, one founder leaves to join Google. They keep their 33%. The company raises seed, then Series A. The departing founder owns 25% post-dilution and adds no value, creating significant resentment.

Investors see this and think:

- These founders don’t understand basic startup mechanics

- They can’t have difficult conversations

- The remaining founders will resent each other

- We’re funding someone who doesn’t work here

What happens: Deal dies, or investors demand fixing it, which means:

- Remaining founders ask departed founder to give back most equity

- Departed founder says no or demands buyout they can’t afford

- Negotiations stall, relationships implode, round collapses

Actual outcome I witnessed: Series A investor walked away. Company eventually shut down without funding. Departed founder kept 25%. Nobody won.

What Investors Will Demand If You Don’t Have It

☑ Four-year vesting schedules with one-year cliffs for all founders

☑ Acceleration clauses for acquisitions (typically single-trigger or double-trigger)

☑ Clear buyback provisions for departing founders (right to repurchase unvested)

☑ Documentation of how initial equity splits were determined

☑ Board approval of any modifications to vesting terms

Founder Vesting Implementation Checklist

Week 1-2: Legal Preparation

- [ ] Hire startup attorney (Orrick, Cooley, Wilson Sonsini level)

- [ ] Draft vesting agreements for all founders

- [ ] Standard terms: 4-year vest, 1-year cliff, monthly vesting thereafter

- [ ] Calculate retroactive vesting credit for time already served

- [ ] Prepare board meeting agenda for approval

Example retroactive calculation:

- Founders been working 18 months

- On 4-year schedule, 18 months = 37.5% vesting credit

- Going forward: remaining 62.5% vests over next 30 months

Week 2-4: Founder Conversations (The Hard Part)

- [ ] Schedule all-hands founder meeting

- [ ] Explain why VCs require vesting (not optional for funding)

- [ ] Show it’s standard for all funded companies (not personal)

- [ ] Frame as protection for everyone (including them)

- [ ] Present retroactive vesting credit (they start partially vested)

- [ ] Get everyone to sign simultaneously (no one-by-one pressure)

Script to use: “We’re implementing 4-year vesting because it’s required for Series A funding. This protects all of us. You’ll get credit for the 18 months you’ve already worked (37.5% vested immediately), and the rest vests monthly over the next 30 months. Every funded company has this. It’s not negotiable if we want to raise capital.”

Week 4-6: Board Approval and Documentation

- [ ] Board meeting to approve vesting arrangements

- [ ] Document in board minutes with rationale

- [ ] All founders sign vesting agreements same day

- [ ] Update cap table showing vested vs unvested shares

- [ ] File all documents with company records

Week 6-8: Cap Table Updates

- [ ] Update cap table software (Carta, Pulley) with vesting schedules

- [ ] Set up automatic monthly vesting calculations

- [ ] Configure cliff dates (typically 1 year from start date)

- [ ] Verify unvested shares shown separately

- [ ] Test departure scenarios (what happens if founder leaves)

Cost: $5,000-$30,000 (legal fees for agreements + board work)

Timeline: 30-90 days depending on founder cooperation

If a Founder Refuses to Sign

You have three options:

Option 1: Negotiate Better Terms

- Offer 3-year vest instead of 4-year

- Offer higher initial vesting credit

- Offer board seat as trade-off

- Explain this is required for fundraising (deal-breaker)

Option 2: Buy Them Out

- If you have capital, purchase their equity now

- Typical: Pay fair market value based on 409A

- Clean break, expensive upfront

- Removes dead equity risk permanently

Option 3: Let Them Leave Without Vesting

- Accept they’ll keep their equity

- Move forward anyway

- Be honest with investors about situation

- Expect valuation reduction of 10-30%

- May kill fundraise entirely

Reality: Option 3 kills most funding rounds. Investors see “founder refused vesting” as massive red flag about team dynamics and business judgment.

Prevention Plan: Vesting from Day One

At Incorporation Checklist:

- [ ] All founders sign vesting agreements simultaneously

- [ ] Standard 4-year vest, 1-year cliff for everyone (including CEO)

- [ ] Board approval in first board meeting

- [ ] Document in formation documents

- [ ] Set up in cap table software from day one

Cost at incorporation: $1,000-$3,000 (included in most formation packages) Cost to retrofit later: $5,000-$30,000 + relationship damage + potential deal death

Common mistake: “We trust each other, we don’t need vesting agreements.”

Reality: Trust doesn’t prevent one founder from leaving after 6 months and keeping 33% of the company. Vesting does.

A pattern I notice across funded B2B tech companies: the best teams address vesting before anyone asks. They understand that vesting isn’t about trust. It’s about aligning incentives.

Mistake #5: Cap Table Management Via Spreadsheet

QUICK ANSWER: Managing your cap table in Excel signals operational immaturity to investors. Common errors: unaccounted SAFEs/convertible notes causing “surprise dilution,” conflicting equity percentages across documents, missing option pool calculations, arithmetic mistakes. During due diligence, cap table errors force deal restructuring and delay closing 14-30 days. Cost to fix: $3K-$15K for professional software + cleanup. Professional platforms: Carta ($2K-$10K/year), Pulley ($1.2K-$6K/year), AngelList (free basic).

Deal Impact: Yellow flag. Delays of 14-30 days indicate operational immaturity.

Fix Cost: $3,000-$15,000 to clean up + software costs ($2,000-$10,000/year)

Fix Timeline: 14-45 days, depending on complexity

If your cap table lives in Excel, your Series A just got more expensive.

Cap table errors don’t just embarrass founders during due diligence. They force deal restructuring, delay closing, and signal to investors that you can’t manage basic financial infrastructure.

According to research from startup legal platform Capbase, poor cap table management raises red flags because it suggests careless financial oversight across the entire business.

Common Cap Table Errors Investors Find

☑ Unaccounted SAFEs or convertible notes from early funding (the “surprise dilution”)

☑ Conflicting equity percentages across different documents

☑ Missing employee option pool calculations

☑ Undocumented verbal equity promises to advisors/early employees

☑ Incorrect dilution modeling for future rounds

☑ Math errors (yes, founders make arithmetic mistakes in Excel)

☑ Missing documentation for every single equity issuance

Each error requires explanation, verification, and often legal reconciliation. This burns time. It burns money. It makes investors question what else hasn’t been managed properly.

Real Example: Cap Table Chaos Costs $165K

Series B company showed investors a cap table with 15M shares outstanding. Legal documents showed 17.5M shares issued. Difference: 2.5M shares (16%) unaccounted for.

Investigation revealed:

- Early SAFE notes converted without updating cap table

- Employee options granted but not recorded

- Advisor equity promised verbally, never documented

- Arithmetic errors in dilution calculations

Cost to fix:

- $12,000 in legal fees to reconcile

- $3,500 for Carta migration and cleanup

- 45-day delay in close

- Investors reduced valuation 8% due to “financial management concerns”

Total impact: $165,000+ in lost valuation + delays

Professional Cap Table Software Comparison

| Platform | Annual Cost | Best For | Key Features | Limitations |

|---|---|---|---|---|

| Carta | $2,000-$10,000 | Series A+ | Industry standard, VC-preferred, full 409A integration, scenario modeling | Expensive, overkill for pre-seed |

| Pulley | $1,200-$6,000 | Seed to Series A | Good balance of features and cost, easy migration, investor-friendly | Less comprehensive than Carta |

| AngelList | Free-$3,000 | Pre-seed to Seed | Free basic version, integrated with AngelList fundraising | Limited advanced features |

| Capbase | $1,500-$5,000 | Formation to Seed | All-in-one (formation + cap table + fundraising) | Limited for complex structures |

Investor preference: Carta is most widely recognized and trusted by VCs. If you can afford it, use Carta. If not, Pulley is an acceptable alternative.

Cap Table Migration Checklist

Week 1: Choose Platform and Gather Documents

- [ ] Select cap table software based on stage and budget

- [ ] Gather every document showing equity issuance:

- Formation documents (certificate of incorporation, bylaws)

- Board minutes approving equity grants

- Stock purchase agreements for all founders

- Employee option grants and exercise records

- SAFE notes and conversion records

- Convertible note agreements

- Advisor equity agreements

- Any other equity promises (written or documented)

Week 2-3: Data Migration

- [ ] Input every transaction chronologically (don’t skip steps)

- [ ] Start with formation (initial founder shares)

- [ ] Add each subsequent equity event in order

- [ ] Include: date, recipient, # shares, price, type (common/preferred/options)

- [ ] Record all SAFEs and convertible notes

- [ ] Calculate conversions accurately

- [ ] Reconcile current ownership percentages

Week 3-4: Verification

- [ ] Compare platform output to your expectations

- [ ] Cross-reference with Delaware filings (authorized shares)

- [ ] Verify option pool math (allocated vs granted vs exercised vs available)

- [ ] Check dilution calculations across all rounds

- [ ] Model next round dilution scenarios

- [ ] Have startup attorney review for accuracy (cost: $1,500-$3,000)

Week 4-5: Ongoing Maintenance Setup

- [ ] Train someone on your team to update after every equity event

- [ ] Set quarterly reconciliation reviews (compare to legal docs)

- [ ] Connect to 409A valuation provider if applicable

- [ ] Maintain clean records of every board approval

- [ ] Set reminders for option exercise windows

- [ ] Configure access for board members and investors

Cost Breakdown:

- Software: $1,200-$10,000/year (ongoing)

- Legal review: $1,500-$3,000 (one-time)

- Migration consulting (if needed): $3,000-$5,000 (one-time)

- Total first year: $5,700-$18,000

Timeline: 14-45 days, depending on transaction complexity

People Also Ask: Cap Tables

What is a cap table, and why do investors care? A capitalization table (cap table) shows all equity ownership in your company: founders, employees, investors, and advisors. It tracks every share issued, option granted, SAFE note converted, and calculates ownership percentages after dilution. Investors care because errors signal poor financial management and can hide “surprise dilution” that reduces their ownership.

Can I use Excel for my cap table? Technically, yes, but investors see it as amateur. Excel cap tables have high error rates (math mistakes, missing transactions, incorrect dilution modeling). For seed stage and beyond, use professional software (Carta, Pulley, AngelList). Cost is $1,200-$10,000/year – far less than the $50K+ you’ll spend fixing errors during due diligence.

How often should I update my cap table? Immediately after every equity event: founder grants, employee option grants, option exercises, new hires getting equity, advisor grants, SAFE conversions, funding rounds. Then, verify quarterly against legal documents. During active fundraising, update weekly as new SAFEs or notes close.

What’s the difference between fully diluted and as-converted? “As-converted” shows current ownership if all preferred stock converts to common (simple cap table). “Fully diluted” includes all potential equity: currently outstanding shares + all unexercised options + all available option pool shares + all convertible notes/SAFEs. Investors always evaluate on a fully-diluted basis.

Do I need a cap table for incorporation? Yes. Your cap table starts the day you incorporate and issue founder shares. Even with 2 founders and no other equity holders, maintain proper records from day one. This prevents expensive reconstruction later and ensures clean documentation for the first employees and investors.

When I’m creating educational email courses for Series A SaaS companies, the framework is always the same: treat your cap table as you would your financial statements. Both tell investors whether you can manage scale.

Prevention Plan: Professional From Day One

At Incorporation:

- [ ] Set up professional cap table software immediately (not later)

- [ ] Input founder equity correctly with vesting schedules

- [ ] Establish quarterly review process

- [ ] Cost: $100-$200/month for basic plan

Ongoing:

- [ ] Update within 24 hours of any equity event

- [ ] Quarterly reconciliation with legal docs

- [ ] Annual attorney review before fundraising

- [ ] Always maintain single source of truth

The math:

- Proper cap table from day one: $2,400/year

- Fixing Excel disaster during Series A: $15,000-$50,000 + 30-60 day delays

- Savings: $12,600-$47,600

Mistake #6: Employee Misclassification (Contractor vs Employee)

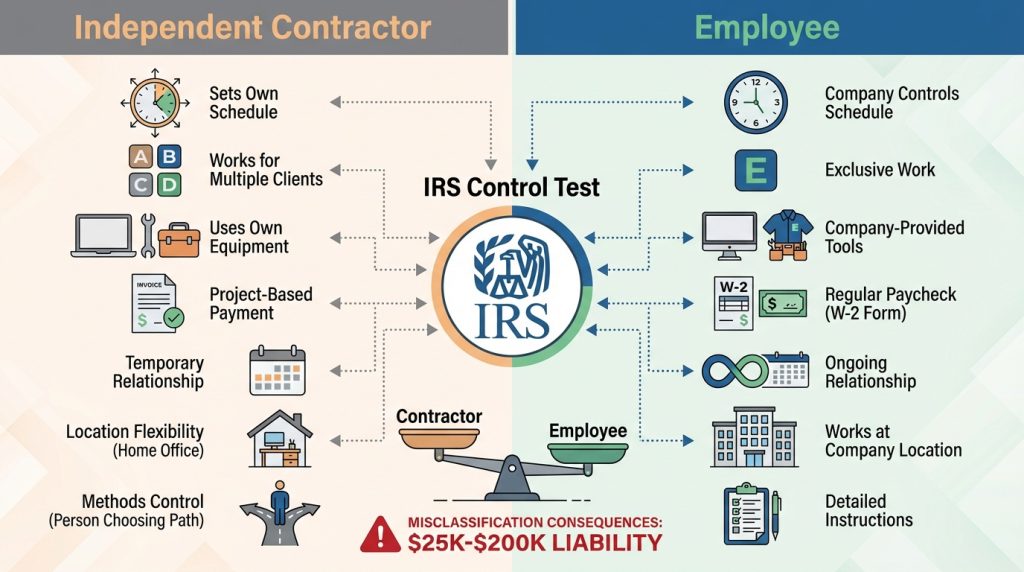

QUICK ANSWER: Calling someone a contractor doesn’t make them one. The IRS applies control tests: if you control hours/schedule, they work exclusively for you, use company equipment, and relationship is ongoing, they’re employees regardless of contract language. Misclassification creates back payroll taxes (7.65%), penalties (up to 40%), state unemployment premiums, and potential lawsuits. Investors calculate total liability during diligence. Cost to fix: $25K-$200K+ depending on scale. Timeline: 60-180 days.

Deal Impact: Yellow flag. Delays of 30-60 days create $10,000-$500,000+ in liability.

Fix Cost: Back taxes, penalties, and legal fees: $25,000-$200,000+ depending on scale

Fix Timeline: 60-180 days to remediate with IRS/state agencies

Calling someone a contractor doesn’t make them one. The IRS and state labor boards don’t care what your agreement says. They care about the actual working relationship.

Misclassifying employees as contractors is one of the most common mistakes startups make. It’s also among the most expensive to remediate during due diligence.

Why Startups Misclassify

Founder thinking: • Contractors = no payroll taxes, no benefits, more “flexibility” • Employees = expensive, complex, permanent • Early-stage founders choose the cheaper path

Why this backfires: • IRS doesn’t accept your classification • State labor boards audit and penalize • Misclassified workers can sue for benefits • Investors won’t fund companies with pending liability

Why Investors Hate Misclassification

When investors discover misclassification during diligence, they calculate:

- Back payroll taxes owed (employer portion: 7.65% of all compensation)

- Penalties for late payment (up to 40% of unpaid taxes)

- State unemployment insurance premiums (retroactive)

- Potential lawsuits from “contractors” claiming employee status

- Legal costs to fix everything ($25,000-$50,000+)

For a company with 8 misclassified workers earning $80K each over 2 years:

- Back payroll taxes: $98,560 (7.65% × $640K × 2 years)

- Penalties (25%): $24,640

- Legal remediation: $30,000

- State unemployment premiums: $15,000

- Total liability: $168,200

This comes directly out of valuation or must be covered before closing.

Real Example: $85K Liability Discovered in Diligence

Series A SaaS company had 8 “contractors” building their product. All worked 40+ hours/week, used company equipment, reported to founders daily, and worked exclusively for the company for 12+ months.

Investors’ classification test: 100% employees, not contractors.

Cost to fix:

- $85,000 in back payroll taxes and penalties

- $30,000 in legal fees to restructure

- $50,000 added to raise to cover liabilities

- 60-day delay in closing

- 5% valuation reduction for “operational risk”

Total impact: $165,000 + delays

IRS Classification Test: Contractor vs Employee

| Factor | Likely Contractor | Likely Employee |

|---|---|---|

| Schedule | Sets own hours, flexible timing | Company controls hours/schedule |

| Clients | Works for multiple companies | Works exclusively for you |

| Equipment | Uses own laptop, tools, software | Uses company-provided equipment |

| Payment | Paid per project or deliverable | Receives regular wages/salary |

| Relationship | Temporary, project-based | Ongoing, indefinite employment |

| Location | Works remotely, their location choice | Works at company office or reports regularly |

| Direction | Determines how to complete work | Receives detailed instructions on methods |

| Integration | Peripheral to core business | Integrated into core business operations |

IRS applies the “degree of control” test across these factors. The more control you have, the more likely they’re an employee.

Worker Classification Audit Checklist

Week 1-2: Audit Current Relationships

- [ ] List every “contractor” currently working for you

- [ ] For each, document:

- How many hours/week do they work?

- Do they work for other companies?

- Do they use their equipment or yours?

- Do you set their schedule or do they?

- Is the relationship temporary or ongoing?

- Do you control how they do the work?

- [ ] Apply IRS control test honestly

- [ ] Identify likely misclassifications

Week 3-4: Reclassify Workers

- [ ] For those who are actually employees:

- Offer proper employment agreements

- Provide W-2 instead of 1099

- Add to payroll with benefits

- Explain change is for compliance

- [ ] For true contractors:

- Restructure relationship to reduce control

- Move to project-based payment

- Allow flexible hours and location

- Update contracts with work-for-hire clauses

Week 4-8: Tax Remediation

- [ ] Calculate back payroll taxes owed for all periods

- [ ] Consult with payroll tax specialist

- [ ] Consider Voluntary Classification Settlement Program (VCSP)

- Reduces penalties if you proactively reclassify

- Pay reduced back taxes (typically 1-year lookback instead of 3)

- [ ] File corrected payroll tax returns (941 forms)

- [ ] Work with payroll provider (Gusto, Rippling) to get current

Week 8-12: Documentation for Investors

- [ ] Employment agreements for all employees (with IP assignment)

- [ ] Proper contractor agreements for true contractors

- [ ] Updated org chart showing employees vs contractors

- [ ] Payroll tax compliance certificates

- [ ] Legal opinion letter confirming clean classification

- [ ] Proof of VCSP participation if applicable

Cost Breakdown:

- Back payroll taxes: $50,000-$150,000 (depends on # workers and duration)

- IRS penalties: $10,000-$40,000 (reduced via VCSP)

- Legal/tax advisor fees: $15,000-$30,000

- Ongoing payroll cost increase: $20,000-$50,000/year (benefits, taxes)

- Total remediation: $95,000-$270,000

Timeline: 60-180 days from audit through IRS remediation

Prevention Plan: Classify Correctly From Day One

When hiring a first person, ask:

- Will they work exclusively for us? → Yes = Employee

- Will we control their schedule? → Yes = Employee

- Will they use our equipment? → Yes = Employee

- Is this ongoing/indefinite? → Yes = Employee

- Will they be integrated into core business? → Yes = Employee

When in doubt, classify as an employee.

The cost of proper classification: $50,000-$75,000/year per employee (salary + taxes + benefits)

The cost of misclassification remediation: $100,000-$200,000 one-time hit + reputation damage

The math:

- Proper employee classification from day one: $75K/year

- Contractor misclassification discovered in Series A: $150K remediation + 60-day delay + 5-10% valuation hit

- Cost of being wrong: $150K-$500K

People Also Ask: Employee Classification

What’s the penalty for misclassifying employees as contractors? IRS penalties: $50 per W-2 not filed, up to 40% of unpaid payroll taxes, plus interest. State penalties vary but can include workers’ compensation fines, unemployment insurance penalties, and wage/hour violations. Total penalties often reach 25-40% of back taxes owed. For a company with $500K in misclassified payments, penalties can range from $ 50K to $100K+.

Can I convert contractors to employees to fix misclassification? Yes, through the IRS Voluntary Classification Settlement Program (VCSP). You proactively reclassify workers as employees and pay reduced back taxes (typically 1 year rather than 3). You must agree to treat workers as employees going forward. This significantly reduces penalties, but you still owe payroll taxes, just for a shorter period.

Do investors always audit employee classification? Yes, it’s standard in legal due diligence for any company with contractors. Investors review: contractor agreements, payment records, work schedules, equipment usage, and relationship duration. They apply IRS tests and calculate potential liability. Large misclassification issues can kill deals or reduce valuations by 10-20%.

A Series B company I’m working with had zero employee misclassification issues. How? Their startup attorney reviewed every contractor agreement before it was signed. $500 legal review prevented $50,000+ liability.

Mistake #7: Privacy Compliance Gaps (GDPR/CCPA for Data Companies)

QUICK ANSWER: B2B SaaS companies processing EU/UK customer data must comply with GDPR (£17M or 4% revenue fines). California customer data requires CCPA ($7,500 per violation). Investors verify: current privacy policy matching business model, GDPR-compliant consent, Data Processing Agreements with customers, security measures, breach procedures. Template privacy policies from 2019 don’t cut it. Cost to build compliant program: $15K-$75K. Timeline: 45-120 days.

Deal Impact: Yellow to Red flag depending on industry. SaaS/data companies: deal killer.

Fix Cost: $15,000-$75,000 for full privacy program buildout

Fix Timeline: 45-120 days for comprehensive compliance

“We’ll get compliant when we need to” is the sentence that ends funding conversations.

For B2B SaaS companies, fintech, healthtech, or any startup processing customer data, privacy compliance isn’t optional. It’s table stakes. Investors won’t fund companies facing potential $20M+ GDPR fines or class-action privacy lawsuits.

What Triggers Investor Scrutiny

Your company processes:

- Data from EU/UK users → GDPR applies (£17M or 4% revenue in fines)

- California resident data → CCPA applies ($7,500 per violation)

- Health data → HIPAA applies (criminal penalties possible)

- Payment data → PCI-DSS applies (can’t process cards without it)

Investors aren’t privacy lawyers, but they know enough to ask:

- “Have you done a privacy impact assessment?”

- “Where’s your Data Processing Agreement template?”

- “Is your privacy policy actually current?”

- “Do you have an EU representative appointed?”

If you can’t answer, they start calculating regulatory risk.

Key Legal Concepts Explained

GDPR (General Data Protection Regulation) is EU/UK privacy law requiring consent for data collection, data deletion on request, breach notification within 72 hours, and Data Processing Agreements with customers. Fines up to £17M or 4% of global revenue.

CCPA (California Consumer Privacy Act) gives California residents rights to know what data is collected, delete data, and opt out of data sales. Fines up to $7,500 per violation. Applies if you have California customers and meet revenue/data thresholds.

Data Processing Agreements (DPAs) are contracts between your company (processor) and customers (controllers) specifying how you handle their data. Required under GDPR for B2B SaaS companies.

Real Example: $60K Privacy Compliance Cost During Series B

Series B SaaS company processed data from EU customers. During diligence, investors found:

- Privacy policy was template from 2019 (outdated by 5 years)

- No GDPR-compliant consent mechanisms

- Data stored in US without EU-approved transfer mechanisms

- No Data Processing Agreements with customers

- No appointed EU representative

- Cookie banners that didn’t actually block cookies

- No data retention or deletion policies implemented

Investor response: Required full privacy remediation before close.

Cost:

- $45,000 for privacy counsel to build compliant program

- $15,000/year for EU representative services (ongoing)

- $8,000 for technical implementation (consent management, data deletion)

- 90-day delay in closing

- 12% valuation reduction for “regulatory risk”

Total impact: $68,000 + 90 days + $600K valuation hit on $5M round

What Investors Actually Examine

☑ Privacy policy matching current business model (not a 2019 template)

☑ Terms of service reflecting actual product functionality

☑ Cookie consent for EU/UK visitors (not just a banner saying “we use cookies”)

☑ Data Processing Agreements (DPAs) template for enterprise customers

☑ Vendor contracts with data processors (AWS, Stripe, analytics tools)

☑ Data retention and deletion policies actually implemented in code

☑ Security measures appropriate for data sensitivity

☑ Breach notification procedures documented and tested

☑ Regular privacy reviews built into product development (privacy-by-design)

Privacy Compliance Program Checklist

- Map all data you collect:

- Personal info: name, email, phone, address

- Payment info: credit cards, bank accounts

- Usage data: login times, features used, IP addresses

- Business data: company info, employee lists

- Special categories: health data, financial data, children’s data

- Identify all jurisdictions:

- Which US states? (California requires CCPA)

- Any EU/UK users? (requires GDPR)

- Other international? (check local laws)

- List all third parties who access data:

- Cloud providers (AWS, Google Cloud, Azure)

- Payment processors (Stripe, PayPal)

- Analytics (Google Analytics, Mixpanel, Amplitude)

- CRM (Salesforce, HubSpot)

- Support tools (Zendesk, Intercom)

- Marketing tools (Mailchimp, Marketo)

- Determine applicable regulations:

- GDPR (EU/UK)

- CCPA (California)

- HIPAA (health data)

- PCI-DSS (payment cards)

- State-specific laws

- Update privacy policy to current practices:

- What data you collect and why

- How you use data

- Who you share data with (all vendors listed)

- User rights (access, deletion, portability)

- Data retention periods

- Contact information for privacy requests

- Last updated date (update quarterly minimum)

- Create GDPR-compliant consent flows:

- Opt-in before data collection (not opt-out)

- Separate consent for different purposes

- Easy to withdraw consent

- Record of consent (who, when, what)

- Draft Data Processing Agreements for customers:

- Use GDPR-compliant template

- Specify data processing terms

- Include security measures

- Address sub-processors

- Cover data transfers outside EU

- Update vendor agreements for GDPR compliance:

- DPAs with AWS, Stripe, all data processors

- Verify they’re GDPR-compliant

- Document sub-processor relationships

- [ ] Implement data deletion on request:

- Build user data export feature

- Build account deletion feature

- Test that data actually deletes (not just flags as deleted)

- Document deletion process and timeline

- [ ] Set up data retention schedules:

- Determine how long to keep each data type

- Automate deletion of old data

- Document retention periods in privacy policy

- [ ] Configure secure data storage:

- Encryption at rest and in transit

- Access controls (who can access what data)

- Logging of data access

- Regular security audits

- [ ] Implement cookie consent for EU visitors:

- Cookie banner with opt-in (not just notice)

- Actually block non-essential cookies until consent

- Cookie policy page listing all cookies

- Use compliant tool (OneTrust, Cookiebot, Osano)

- [ ] Test breach notification procedures:

- Document breach response plan

- Know 72-hour GDPR notification requirement

- Have PR/legal contacts ready

- Test notification process

- [ ] Appoint DPO or privacy lead:

- Internal person or fractional DPO service

- Responsible for privacy compliance

- Contact for privacy requests

- [ ] Schedule quarterly privacy reviews:

- Review privacy policy for accuracy

- Audit data collection practices

- Check vendor compliance

- Update documentation

- [ ] Train team on privacy requirements:

- Engineering: privacy-by-design principles

- Sales: what to say about data security

- Support: how to handle privacy requests

- Everyone: breach reporting procedures

- [ ] Document everything for investor review:

- Privacy policy (current)

- Data Processing Agreements (templates + signed)

- Vendor DPAs (all sub-processors)

- Data map (what data, where stored, how long)

- Security measures (encryption, access controls)

- Privacy training records

- Breach procedures

Cost Breakdown:

- Privacy attorney consultation: $15,000-$30,000

- Cookie consent platform: $3,000-$8,000/year

- EU representative service: $10,000-$15,000/year (if needed)

- Technical implementation: $5,000-$15,000 (developer time)

- DPO service (if outsourced): $8,000-$12,000/year

- Total first year: $41,000-$80,000

Ongoing annual cost: $20,000-$35,000 (compliance maintenance)

Timeline: 45-120 days from assessment through full implementation

People Also Ask: Privacy Compliance

Do I need to comply with GDPR if I’m a US company? Yes, if you process data from EU or UK residents. GDPR applies based on where your users are located, not where your company is incorporated. Even one EU customer triggers GDPR obligations. Fines up to €20M or 4% of global revenue, whichever is higher.

What’s the difference between GDPR and CCPA? GDPR (EU/UK) requires opt-in consent before data collection and applies to all personal data. CCPA (California) gives consumers rights to know/delete/opt-out but doesn’t require opt-in consent. GDPR is stricter. If you’re GDPR-compliant, CCPA is easier. Both have significant fines for violations.

What is a Data Processing Agreement, and when do I need one? A DPA is a contract between you (the data processor) and your customer (the data controller) that specifies how you handle their data. Required under GDPR for any B2B SaaS company processing customer data. Enterprise customers will demand signed DPAs before using your product. Have a GDPR-compliant template ready.

How much do privacy violations actually cost? GDPR fines: British Airways £20M (2019), Google €90M (2022), Meta €390M (2023). CCPA settlements: Sephora $1.2M (2022). Beyond fines: legal costs ($100K-$500K), customer churn (30-50% after breach), valuation damage during fundraising (10-20% reduction). Cost of compliance ($40K-$80K) is far less than cost of violation ($500K-$10M+).

Do investors actually check privacy compliance? Yes, especially for B2B SaaS, fintech, and healthtech. Standard due diligence includes: reviewing the privacy policy, checking the DPA template, verifying GDPR consent mechanisms, auditing vendor contracts, and assessing security measures. For data-heavy companies, investors may require a third-party privacy audit before investment. Large gaps can kill deals or reduce valuations by 10-20%.

Prevention Plan: Privacy-by-Design From Day One

- [ ] Build a compliant privacy policy before collecting data

- [ ] Implement GDPR-style consent (opt-in, not opt-out)

- [ ] Use privacy-friendly analytics (can anonymize IPs, respect DNT)

- [ ] Encrypt data at rest and in transit

- [ ] Build data export and deletion features into the product

- Privacy review before every new feature launch

- Update privacy policy quarterly

- Annual security audit

- Provide regular privacy training for the team

Cost of doing it right from day one: $10,000-$20,000 initial + $15,000-$25,000/year ongoing

Cost of retrofitting during fundraising: $40,000-$80,000 + 60-120 day delays + valuation risk

When developing content strategies for funded startups, this pattern often appears: founders treat privacy as legal paperwork rather than a product feature.

Proper privacy compliance means:

- Privacy-by-design in product development

- Current privacy policies reviewed quarterly

- Customer DPAs for enterprise contracts

- Security practices matching data sensitivity

- Regular legal reviews (annual minimum)

A cleantech client recently faced this during their Series B raise. They had excellent technology and strong unit economics. During due diligence, investors discovered their privacy policy was a template from 2019, unchanged despite significant product evolution and European expansion.

The compliance gap didn’t just delay the round. It reduced the valuation because investors factored in remediation costs plus the legal risk of operating with inadequate compliance infrastructure.

This tracks with what I see in the LinkedIn strategies I develop for B2B tech CEOs: regulatory compliance is a competitive moat. Companies that build compliance into their operational DNA move faster because they’re not constantly playing catch-up with legal requirements.

Mistake #8: Stock Not Formally Issued (The Offer Letter Trap)

QUICK ANSWER: Promising equity in an offer letter doesn’t mean stock was legally issued. Proper issuance requires: board approval documented in minutes, stock issued at fair market value (409A valuation), signed stock purchase agreements, and cap table updates. Skip these steps and try to fix years later = founders owe taxes on current valuation. Example: Company worth $500K at founding, now worth $10M at Series A. Issue stock now = founder owes tax on $2.5M “income” with $0 cash. Cost to fix: $10K-$100K + potential six-figure tax bills.

Deal Impact: Red flag. Creates phantom tax liabilities, delays close 30-90 days.

Fix Cost: $10,000-$100,000 in legal fees + potential six-figure tax bills for founders

Fix Timeline: 30-90 days to properly issue and document

Promising someone equity is not the same as issuing stock. Investors have seen this mistake repeatedly kill deals: during diligence, founders discover that they never actually issued stock to themselves or early team members.

According to SPZ Legal’s startup practice (April 2025 blog post), they’ve seen companies raise funding without having actually issued stock to founders. The offer letter promising equity isn’t enough. Neither is a verbal agreement or even a signed employment contract mentioning equity.

What Actually Must Happen to Issue Stock

☑ Board must approve the issuance (documented in board minutes)

☑ Stock must be issued at fair market value (supported by 409A valuation)

☑ Proper legal agreements must be signed (stock purchase agreement, vesting agreement)

☑ Stock certificates or cap table must reflect issuance

☑ Filing with Delaware (or relevant jurisdiction) if required

☑ 83(b) election filed within 30 days (for vesting stock)

Why This Matters: The Tax Bomb Example

Year 1: Founders “agree” to 25/25/25/25 split. No formal issuance. Company is worth $500K.

Year 3: Company raising Series A at $10M valuation. Lawyers discover stock was never formally issued.

Fix attempt: Issue stock now at $10M valuation.

Tax consequence: Each founder receives $2.5M in stock value, owes income tax on $2.5M (~$1M tax bill each), has $0 cash.

The correct approach: Issue stock in Year 1 at low/zero valuation when company is worth $500K. Pay tax on $125K value (~$50K total tax bill for all founders) OR issue as vesting stock with 83(b) election and pay $0-$500 tax total.

Cost difference: $4M in unnecessary taxes vs $2,000 in proper formation costs.

What Investors Find During Diligence

- Stock ledger doesn’t match what founders claim to own

- No board minutes approving equity issuances

- Missing stock purchase agreements

- Verbal promises to advisors/early employees never documented

- Founders who think they own 25% but don’t legally own anything

Stock Issuance Remediation Checklist

- Hire a startup attorney (Orrick, Cooley, Wilson Sonsini level – not generalist)

- Identify everyone who should own stock but doesn’t have proper documentation:

- Founders

- Early employees promised equity

- Advisors granted equity

- Consultants given equity

- Determine “should have issued” dates and valuations:

- When did the founder start working? (Use that date and valuation)

- When did the employee join? (Use that date and valuation)

- What was the company worth then? (May need retrospective 409A)

- [ ] Schedule emergency board meeting

- [ ] Approve each equity issuance retroactively:

- Ratify all founder grants

- Approve employee equity grants

- Approve advisor grants

- Use proper valuations for each date

- [ ] Document everything in clean board minutes

- [ ] Have all board members sign minutes

- [ ] Execute stock purchase agreements for everyone:

- Founders

- Employees

- Advisors

- [ ] Issue stock certificates or update cap table ledger

- [ ] File any required state documents (Delaware stock ledger)

- [ ] Obtain 409A valuations for all issuance dates:

- May need retrospective valuations for past dates

- Cost: $2,000-$5,000 per valuation

- Required to defend stock prices to IRS

- Calculate tax implications for all recipients:

- If issuing at current high valuation = phantom income tax

- May be able to issue as vesting with 83(b) (if within 30 days)

- Consider grossing up compensation to cover taxes

- File any corrected tax forms:

- W-2 corrections for employees

- 1099 corrections for advisors/consultants

- Consult with tax attorney on minimizing tax impact

- Document everything for investor review:

- Tax calculations

- Remediation steps taken

- Compliance with IRS rules

- Implement formal equity issuance process:

- Board approval required before any equity promise

- Stock purchase agreement template ready

- 83(b) election template ready

- Quarterly cap table review

- Require board approval before any equity promise

- Template all equity documentation (standardize)

- Review cap table quarterly for discrepancies

- Never make verbal equity promises (written only)

Cost Breakdown:

- Legal fees: $15,000-$50,000 (depends on complexity)

- Retrospective 409A valuations: $4,000-$15,000 (multiple valuations)

- Tax advice: $5,000-$10,000

- Potential tax liability for recipients: $0-$500,000+ (depends on when issued vs when should have issued)

- Total: $24,000-$575,000+

Timeline: 30-90 days minimum

Prevention Plan: Issue Stock Formally at Incorporation

- [ ] Hold first board meeting

- [ ] Board approves initial founder stock issuance

- [ ] Document in board minutes (dated, signed)

- [ ] Execute stock purchase agreements (all founders sign)

- [ ] Set stock price (typically $0.001-$0.01 per share at incorporation)

- [ ] Issue stock certificates or update cap table

- [ ] All founders file 83(b) elections within 30 days

- [ ] Cost: $0-$1,000 (usually included in formation)

- Board approval before every equity grant

- 409A valuation determines fair market value (required)

- Stock purchase agreements signed before issuance

- 83(b) elections filed within 30 days for vesting stock

- Cap table updated immediately after each issuance

The board meeting to approve stock issuance takes 15 minutes. Fixing improper issuance years later costs $50,000+.

Proper stock issuance means:

- Board approves every equity grant (even to founders)

- 409A valuation determines fair market value

- Stock purchase agreements signed

- 83(b) elections filed within 30 days (for vesting stock)

- Cap table updated immediately

Investors see a missing proper stock issuance and immediately think: “These founders don’t understand corporate governance basics. What else have they done wrong?”

💡 CONTRARIAN INSIGHT

Common belief: “We all agreed to the equity split, that’s enough. We’ll do the paperwork later.”

Reality from 500+ podcast interviews with funded CEOs: Legal ownership follows documentation, not agreements. I’ve seen three companies where founders “agreed” to equity splits but never formally issued stock. Years later during acquisitions, one founder claimed they never actually received stock and demanded renegotiation. Two deals died. One paid $500K settlement to the departing founder.

Why this matters: Verbal agreements and handshake deals have zero legal value. During acquisition or investor due diligence, only properly issued and documented stock counts. Everything else is a liability.

Mistake #9: Using the Wrong Type of Lawyer (Your Uncle’s Cousin)

QUICK ANSWER: Startup law is specialized. Generic corporate lawyers create wrong documents that investors reject. VCs expect standardized documents: NVCA model docs, Y Combinator SAFEs, Series Seed templates. Using your uncle’s cousin who does real estate law costs $0 upfront but $20K-$100K to fix during fundraising when you need to redo everything. Use top startup firms (Orrick, Cooley, Wilson Sonsini) for $10K-$20K or legal tech platforms (Carta Launch, Clerky, Capbase) for $1K-$5K. Never use generic lawyers.

Deal Impact: Yellow to Red flag. Wrong documents = deal collapse.

Fix Cost: $20,000-$100,000 to redo everything properly + wasted fees to wrong lawyer

Fix Timeline: 30-120 days to clean up, may kill active fundraise

“My uncle’s cousin is a lawyer and will do it for free” is how you end up with legal documents that investors refuse to accept.

Startup law is a niche. According to Capbase’s research on common legal mistakes, even lawyers who understand corporate and business law often lack familiarity with the nuances of venture financing and startup-specific structures.

The Problem with Generic Lawyers

What generic corporate lawyers do:

- Use standard LLC operating agreements (not VC-compatible)

- Create employment contracts without IP assignments

- Issue equity without vesting or 83(b) elections

- Don’t understand 409A valuations

- Never heard of SAFE notes or QSBS

- Use non-standard terms that confuse investors

What VCs expect:

- Delaware C-Corp with standard certificate of incorporation

- NVCA (National Venture Capital Association) model documents

- Y Combinator SAFE notes for seed funding

- Series Seed documents for early rounds

- Proper founder vesting (4-year, 1-year cliff)

- IP assignments from everyone

- 83(b) elections filed

When investors see non-standard documents, they think:

- This will be expensive to fix

- What other mistakes are hiding here?

- These founders don’t understand the VC ecosystem

- We’ll waste months in legal cleanup

Real Example: $45K to Fix “Free” Legal Work

Seed-stage SaaS company used family friend (real estate attorney) to incorporate and issue founder equity.

What he created:

- Standard LLC operating agreement (not Delaware C-Corp)

- Generic employment contracts without IP assignment clauses

- Equity agreements without vesting schedules

- No 83(b) elections filed

- No stock purchase agreements

- No board minutes documenting anything

What VCs required during Series A diligence:

- Convert LLC to C-Corp (triggering tax events)

- Reissue all equity properly with vesting

- Redo all employment agreements with IP assignments

- Reconstruct cap table from scratch

- Create 2 years of retroactive board minutes

- Get 409A valuations for all equity grants

Cost: $45,000 in proper startup attorney fees to fix everything

Timeline: 90-day delay in fundraising

Lost momentum: Competing startup raised during delay

Result: Deal eventually closed at 15% lower valuation due to “operational concerns”

Legal Resource Comparison: What to Actually Use

| Option | Cost | Best For | Pros | Cons |

|---|---|---|---|---|

| Top Startup Firms (Orrick, Cooley, Wilson Sonsini, Gunderson Dettmer, Goodwin) | $10K-$20K seed to Series A | Seed through Series C+ | VC-standard docs, investor recognition, deep expertise | Expensive for pre-seed |

| Legal Tech Platforms (Carta Launch, Clerky, Capbase) | $1K-$5K for formation + fundraising | Pre-seed to Seed | Affordable, automated, standardized templates | Limited for complex issues, edge cases |

| Fractional Legal (like Intellectual Strategies) | $5K-$15K per engagement | Seed to Series B | Strategic guidance + affordable, flexible | Not full-service law firm |

| Generic Corporate Lawyer | $0-$15K | NEVER | Cheap or free | Wrong documents, expensive to fix later ($20K-$100K) |

Who You Should Actually Use: Top Startup Law Firms

These firms know VC market standards and use documents investors recognize:

- Orrick: Industry standard, used by top VCs globally

- Cooley: Strong startup practice, excellent for Series A+

- Wilson Sonsini: Silicon Valley staple, gold standard

- Gunderson Dettmer: Startup-focused, emerging company specialists

- Goodwin: Growing startup practice, strong in tech/life sciences

Why these firms?

They use standardized documents VCs recognize:

- Series Seed documents (industry standard for first institutional round)

- Y Combinator SAFE notes (standard for pre-seed/seed)

- NVCA (National Venture Capital Association) model documents (Series A+)

When investors see these familiar documents, diligence moves faster. No questions about “why is this clause different?” or “what does this non-standard term mean?”

Typical costs:

- Formation (C-Corp + founder docs): $3,000-$5,000

- First employee package (templates): $1,000-$2,000

- SAFE note round: $5,000-$8,000

- Series Seed round: $15,000-$25,000

- Series A round: $25,000-$50,000

Alternative: Legal Tech Platforms (If You Can’t Afford $15K)

If you can’t afford $15,000-$30,000 in legal fees, use software designed for startups:

Carta Launch

- Automated Delaware C-Corp formation

- Includes: incorporation docs, founder stock, vesting agreements, board minutes

- Cap table software included

- Cost: $500-$1,500

Clerky

- Handles formation, equity issuance, fundraising docs

- Templates for SAFEs, option grants, board consents

- Well-documented process

- Cost: $1,000-$3,000

Capbase

- All-in-one: formation through Series A fundraising

- Compliance monitoring included

- Basic cap table management

- Cost: $1,500-$5,000

Cost comparison:

- Traditional generalist lawyer: $5,000-$15,000 (wrong docs, expensive to fix)

- Top startup firm: $10,000-$20,000 (right docs, investor-ready)

- Legal tech platform: $1,000-$5,000 (right docs, limitations on complexity)

All three options provide the required documents. Never use a generic corporate attorney at any price.

Legal Cleanup Checklist (If You Already Used Wrong Lawyer)

- Hire proper startup attorney for review

- Provide all existing legal documents:

- Formation documents

- Employment agreements

- Equity agreements

- Fundraising documents

- Cap table

- Board minutes

- Attorney identifies all non-standard or incorrect documents

- Prioritize what must be fixed before fundraising (red flags first)

- If wrong entity type (LLC/S-Corp):

- Convert to C-Corp (see Mistake #1)

- Cost: $50,000-$200,000

- Fix cap table errors:

- Migrate to professional software

- Reconcile all equity issuances

- Cost: $3,000-$15,000

- Reissue equity with proper vesting:

- Board approval

- Vesting agreements

- 83(b) elections (if not too late)

- Cost: $5,000-$30,000

- Update employment agreements:

- Add IP assignment clauses

- Ensure proper classification (employee vs contractor)

- Use startup-standard templates

- Cost: $3,000-$10,000

- Create missing board minutes:

- Retroactive minutes for all major decisions

- Document equity grants

- Ratify prior actions

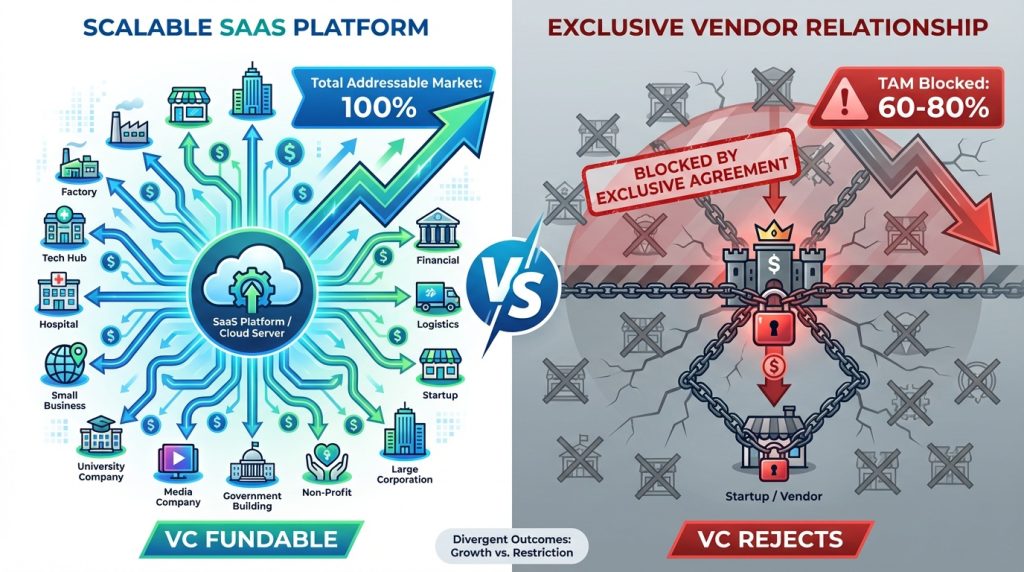

- Cost: $2,000-$5,000